Introduction to Blocksize

Blocksize is the market leader in on-chain market data products and Node Infrastructure for Staking and Decentralized Oracle Nodes. Blocksize leverages their unique positioning as Data Publisher in Decentralized Oracle Networks to access high yield staking and publisher rewards.

Blocksize has implemented a delta-neutral self-staking strategy designed to underline the integrity of its on-chain price feeds and it’s dedication to high-performance Node Infrastructure, which will unlock high yield opportunities in the staking market for investors.

Blocksize isolates Staking Yields from price fluctuations through the use of delta hedging derivatives positions against spot positions, maintaining a relatively stable value with reference to the value spot crypto assets as well as futures positions.

Strategy Yield Sources

Decentralized Oracle Networks and Staking Networks incentivize Node Operator to secure their price feeds and validator infrastructure with own funds to ensure aligned interests and integrity of participants. More stake leads to higher Network integrity leads to higher rewards of network participants with high delegations.

The Blocksize delta-neutral self-staking strategy generates yield from 3 Sources:

Rewards from publishing price data on-chain through Decentralized Oracle Nodes and On-chain Data Publishers

Commissions & operational network rewards generated by own Staking Nodes

Funding and basis spread earned from the delta hedging derivatives positions

The yield is generated from three sustainable, exogenous sources. In addition, investment risks are mitigated by an algorithmic management of the investment strategy.

Staking Rewards (Yield Source No. 1 & 2)

We self-stake assets to Blocksize Decentralized Oracle Nodes and Validator Nodes. The rewards / yield is generated through:

Paid rewards for successful publication of e.g. ETH/USD price on-chain.

Consensus layer inflationary rewards (Staking Rewards).

Execution layer fees (Block Rewards).

MEV capture (MEV Rewards) paid to Validators.

Commissions earned from 3rd Party stake delegated to Blocksize Validators and Oracle Nodes.

Funding Rate from derivates position (Yield Source No. 3)

All invested assets will be hedged with a corresponding short derivatives positions to hedge the delta of the staked assets. Historically due to the mismatch between demand & supply for exposure to digital assets, there has been a positive funding rate & basis spread earned by participants who are short this delta exposure. Details about Funding Rates can be found in section Funding Rate .

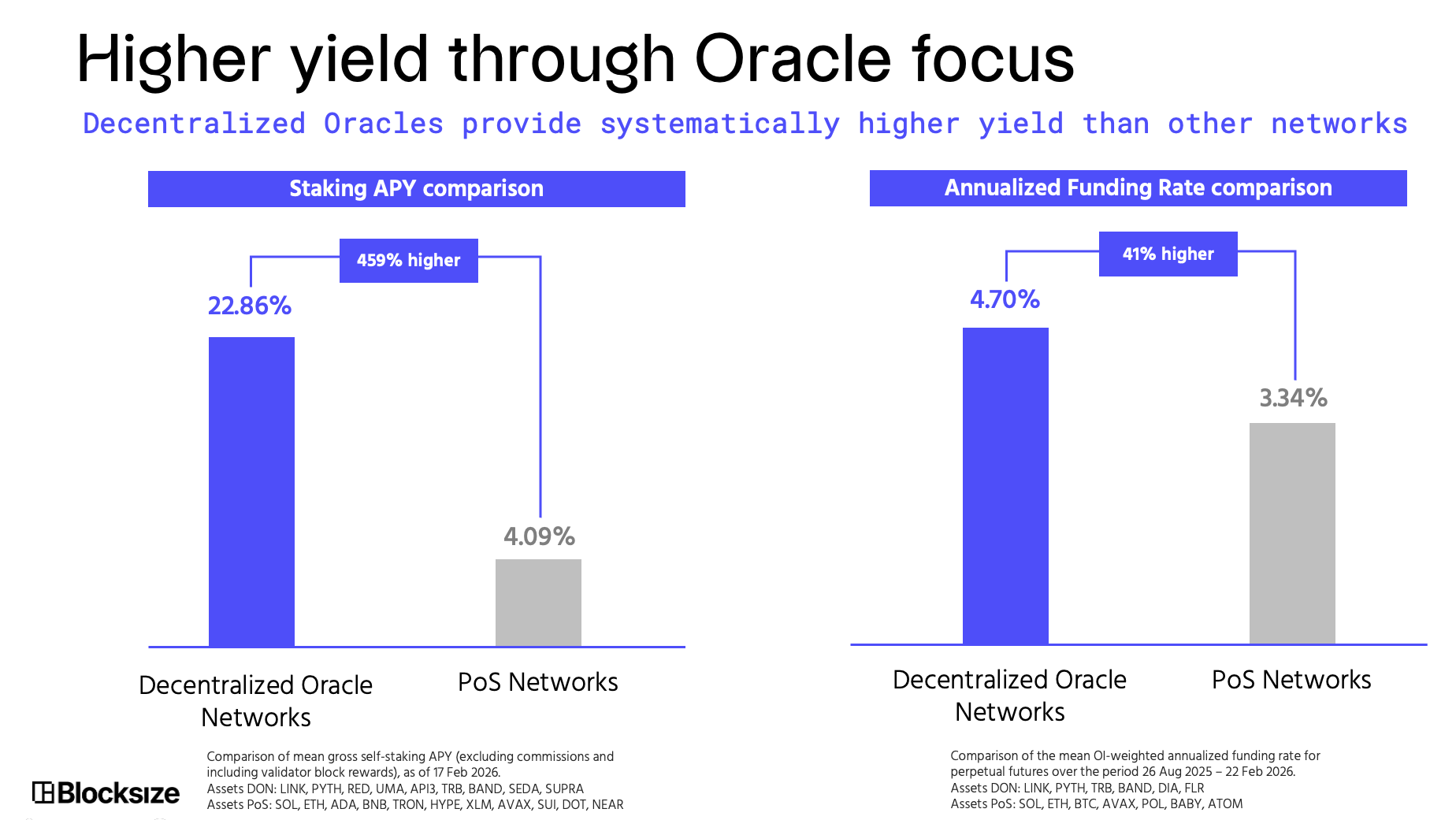

Decentralized Oracles as superior Yield Source

Delta-Neutral Self-Staking Strategy

Blocksize’s delta-neutral self-staking strategy is built around three core ideas:

Self-stake high-quality oracle tokens and validator assets to earn staking and protocol rewards.

Neutralize market beta by hedging spot exposure with short perpetual futures, earning funding fee where available.

Reduce tail and venue risks using systematic controls, including automated risk management tools and Option Overlay designed to protect the portfolio in severe stress events.

Blocksize runs a delta-neutral, yield-oriented managed strategy focused on Decentralized Oracle Networks and selective validator assets.

At a high level:

The portfolio holds spot positions in tokens of Decentralized Oracle Networks and selected Proof-of-Stake Networks, including Liquid Staking Tokens.

Spot positions are staked (and, where applicable, used for oracle data publishing).

Market price risk is hedged using short perpetual futures

The strategy earns yield from:

Oracle staking & data publishing rewards

Validator/staking rewards

Perpetual funding rates** (when positive)

A tail hedge program is maintained to reduce “hedge failure” (e.g. ADL) risk in severe market drawdowns.

What Makes Blocksize Unique?

Securing on-chain price feeds with capital opens superior yield opportunities to stakers. However, technology companies providing accurate on-chain data feeds, usually lack the capital to fully capitalize on this opportunity. Vice-versa institutional investors lack the competence and technology to access such high yield staking opportunities through operating Decentralized Oracle Nodes and providing on-chain data feeds. Blocksize addresses this problem by allowing institutional investors to access such unique staking yields through Blocksize’s delta-neutral self-staking strategy. Blocksize offers the first yield bearing strategy leveraging the Decentralized Data Economy through their Decentralized Oracle Nodes.

Blocksize operates market data infrastructure and decentralized oracle node operations. This enables Blocksize to act as a data publisher and/or node participant across multiple oracle ecosystems.

In addition to staking rewards, oracle ecosystems may pay for:

Publishing market data

Maintaining oracle availability and quality

Participation in oracle security mechanisms

These revenues can be distinct from “generic staking” returns.

Many yield strategies rely primarily on:

L1 staking (often low single-digit yields), and/or

market-neutral carry without oracle-native revenue.

Blocksize’s core differentiation is access to oracle-native revenue streams that depend on publisher/node participation, not only staking rewards from token inflation.

Portfolio Assets

Tellor

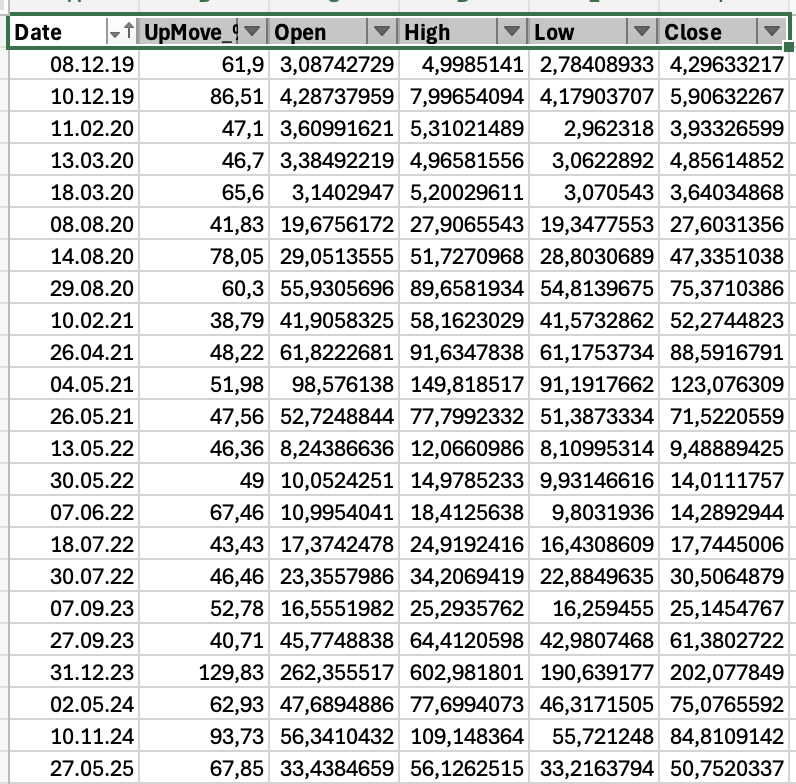

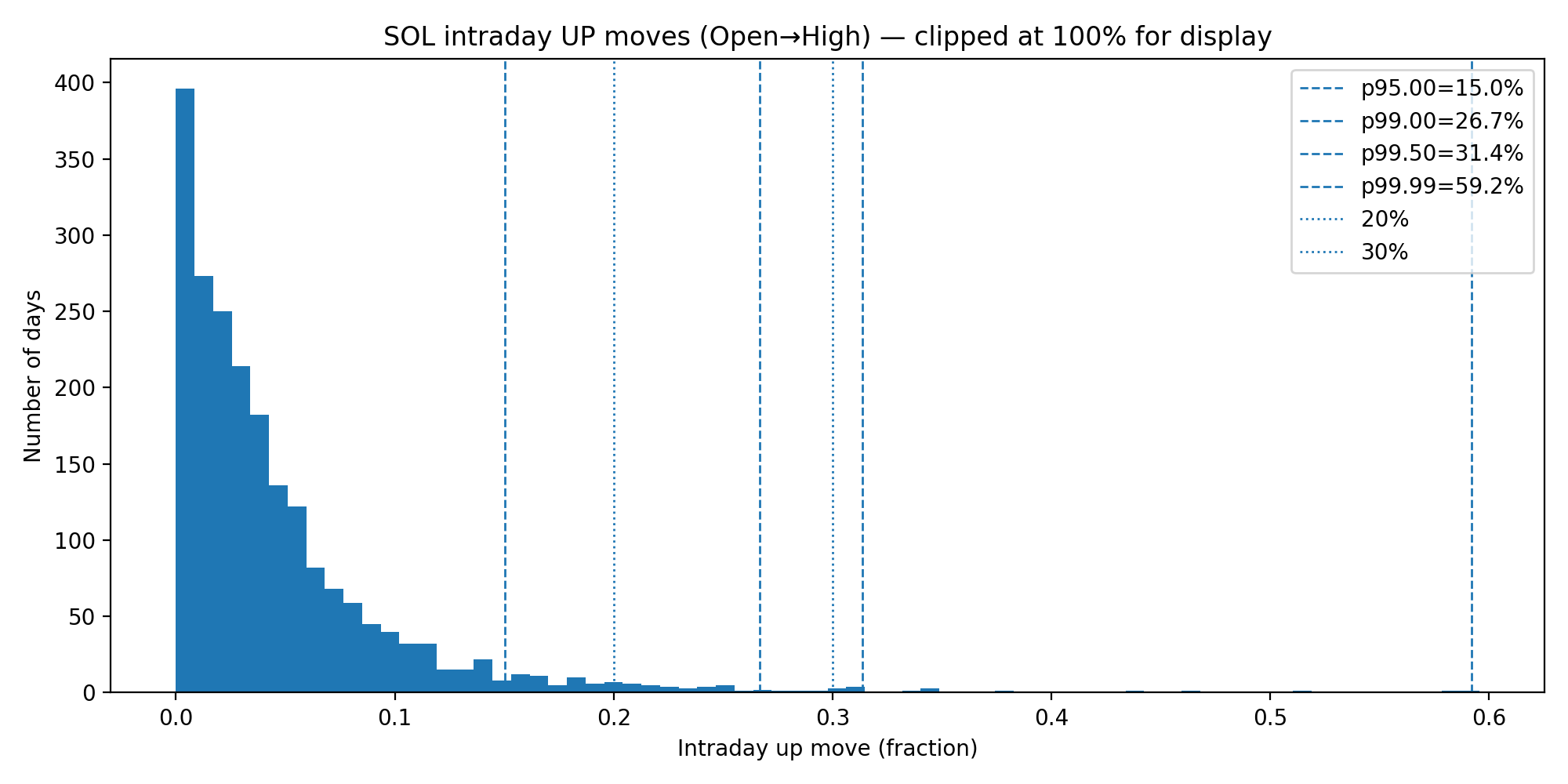

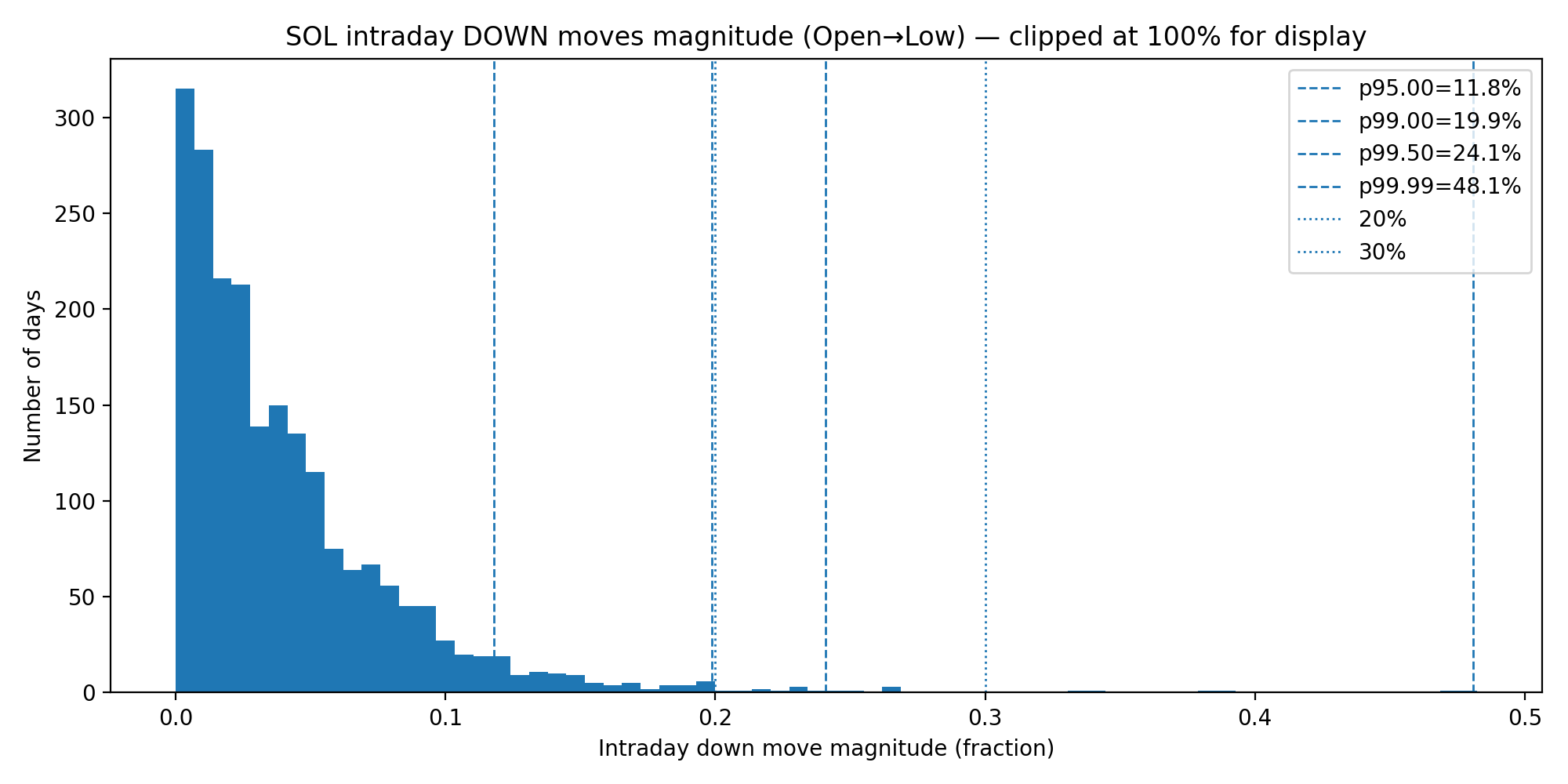

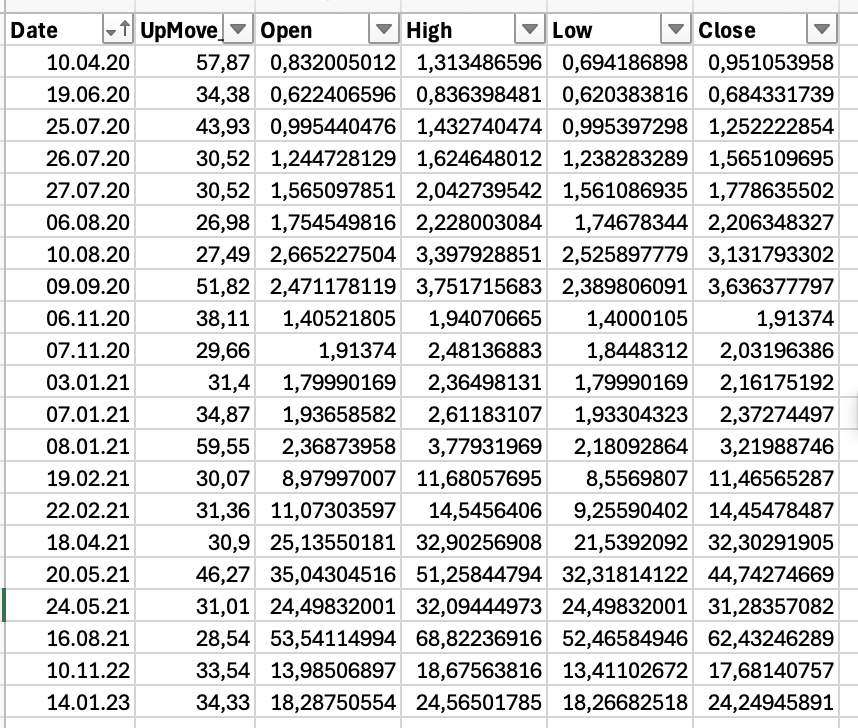

Solana

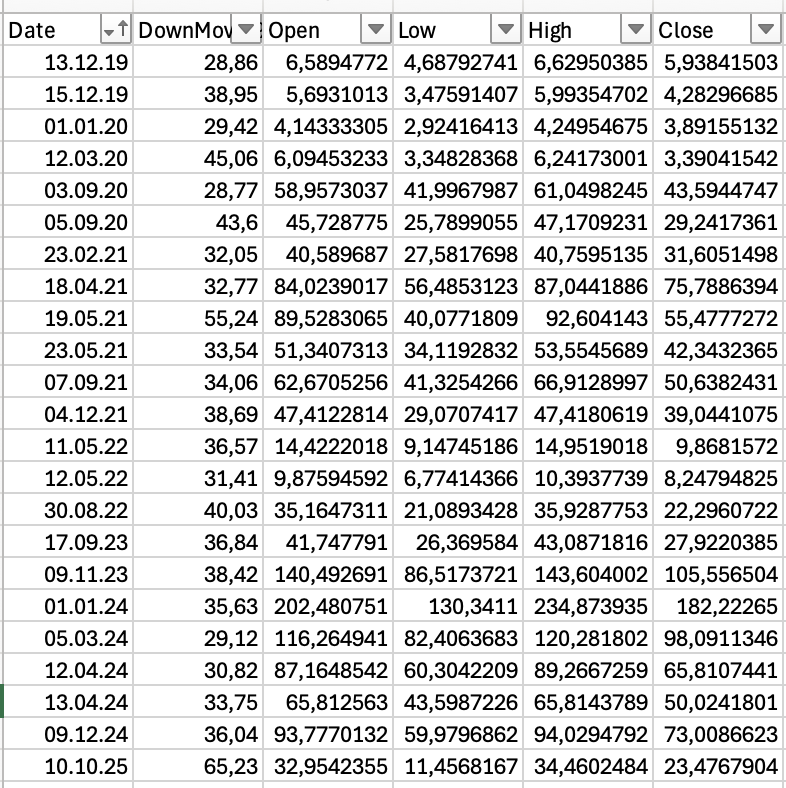

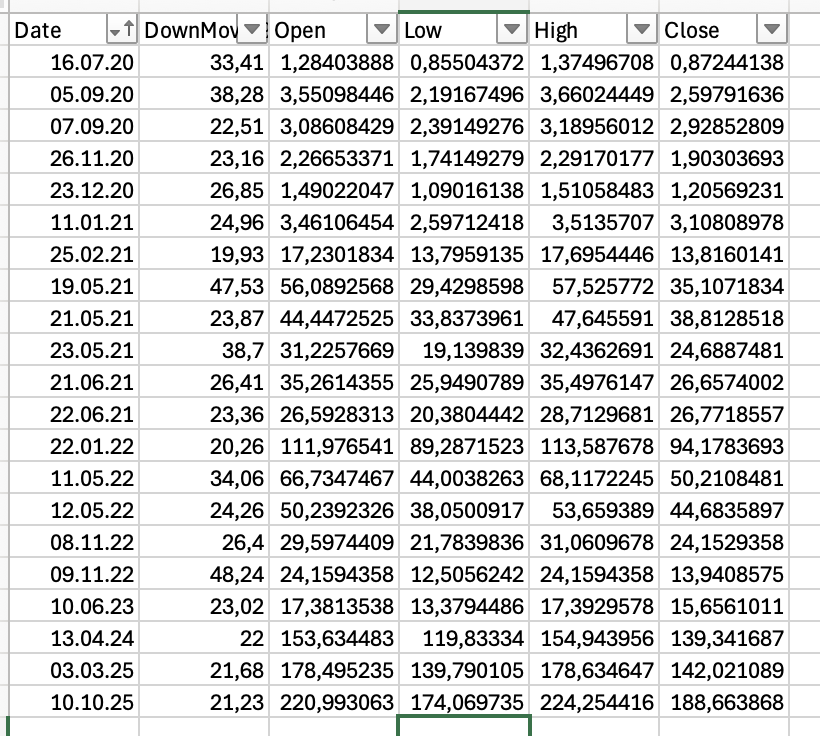

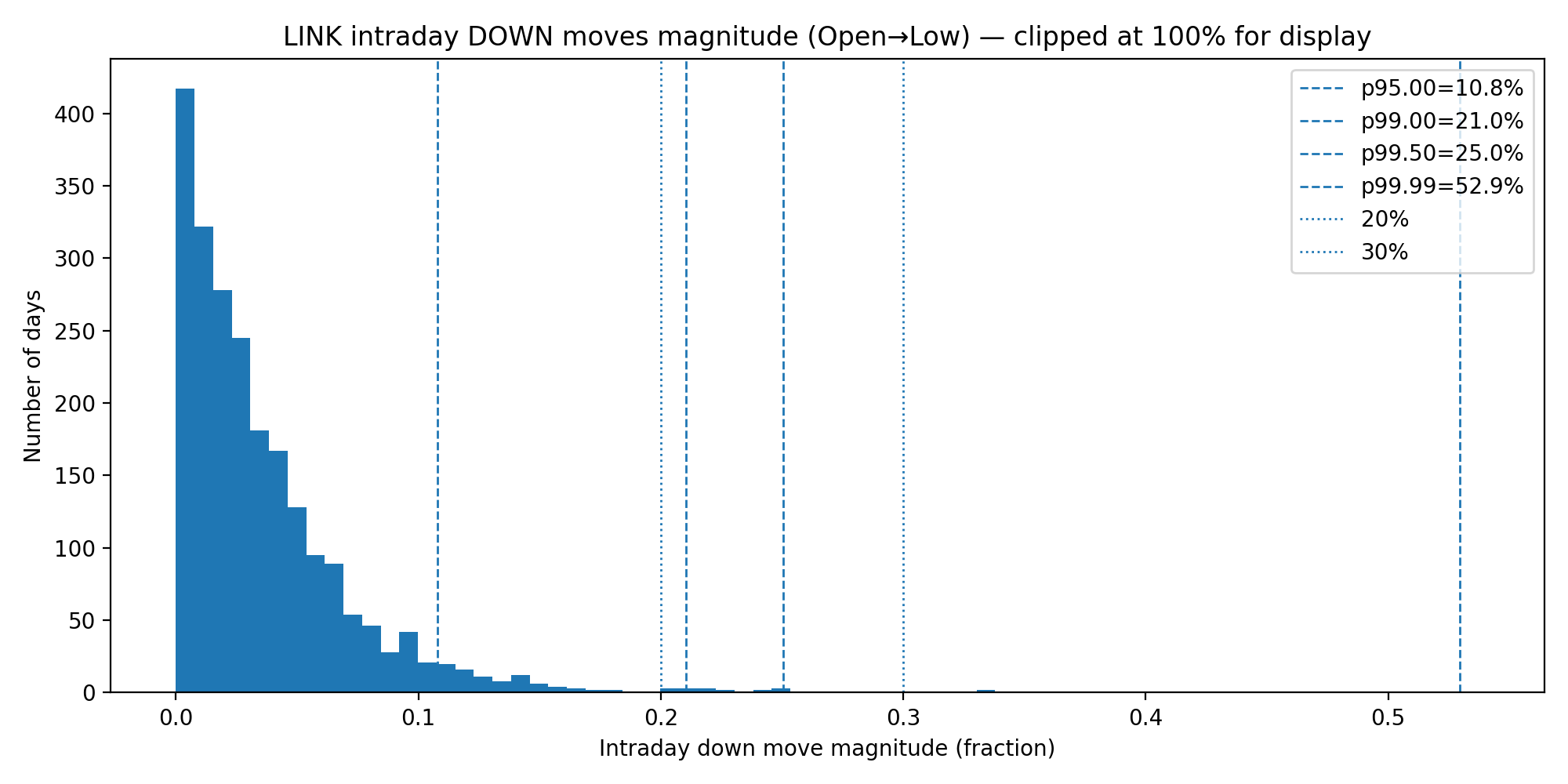

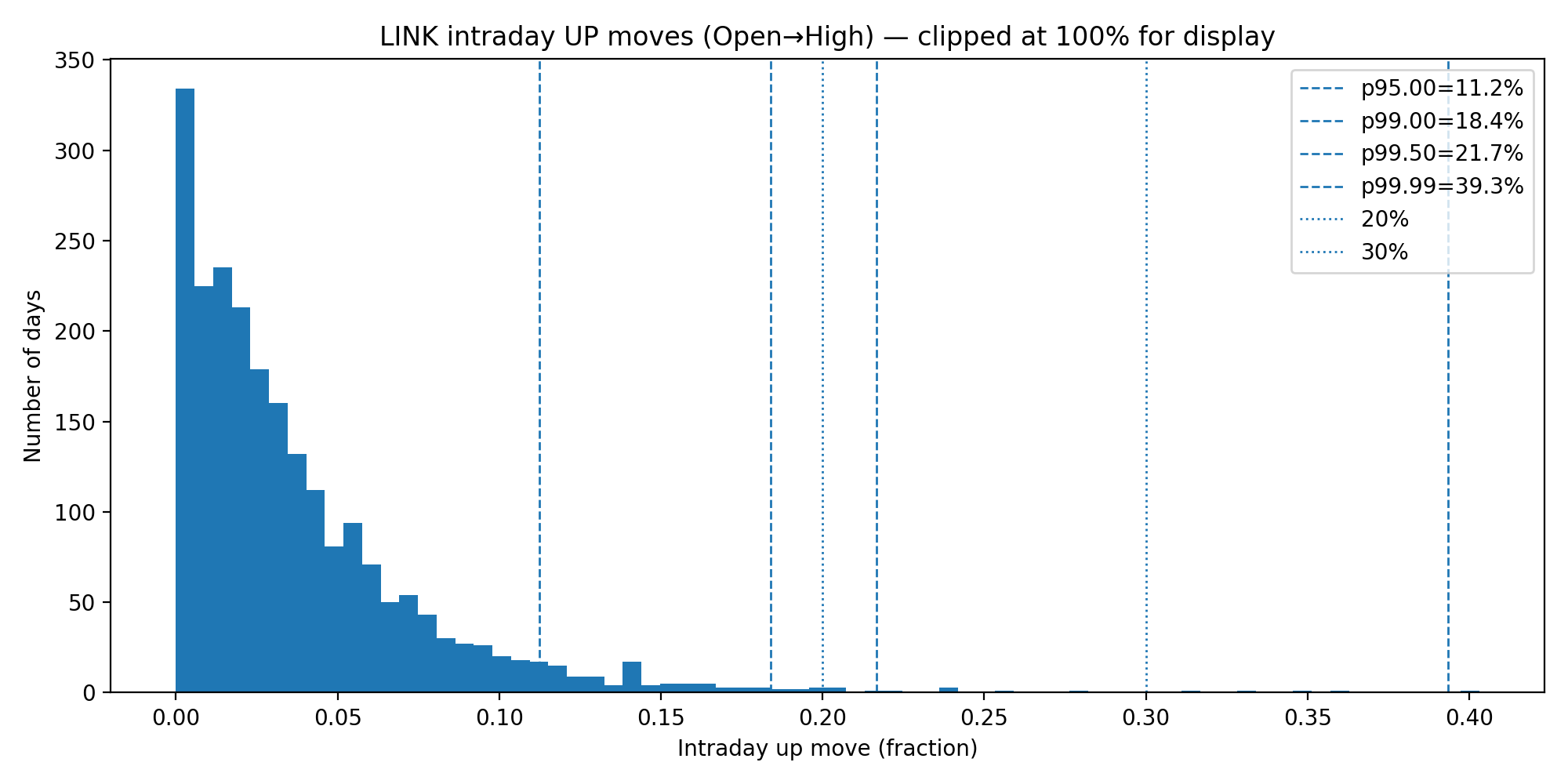

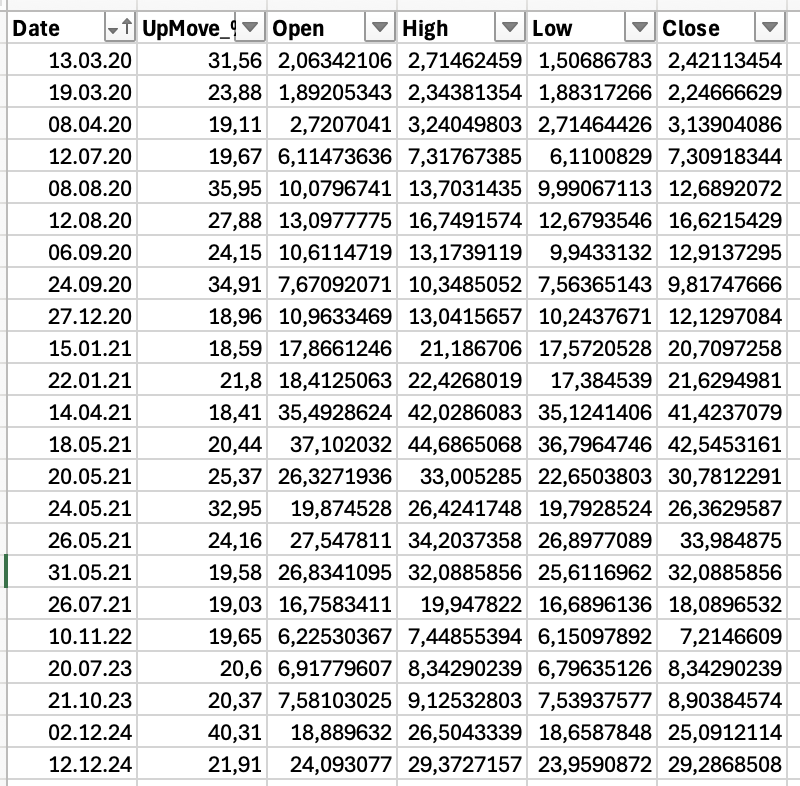

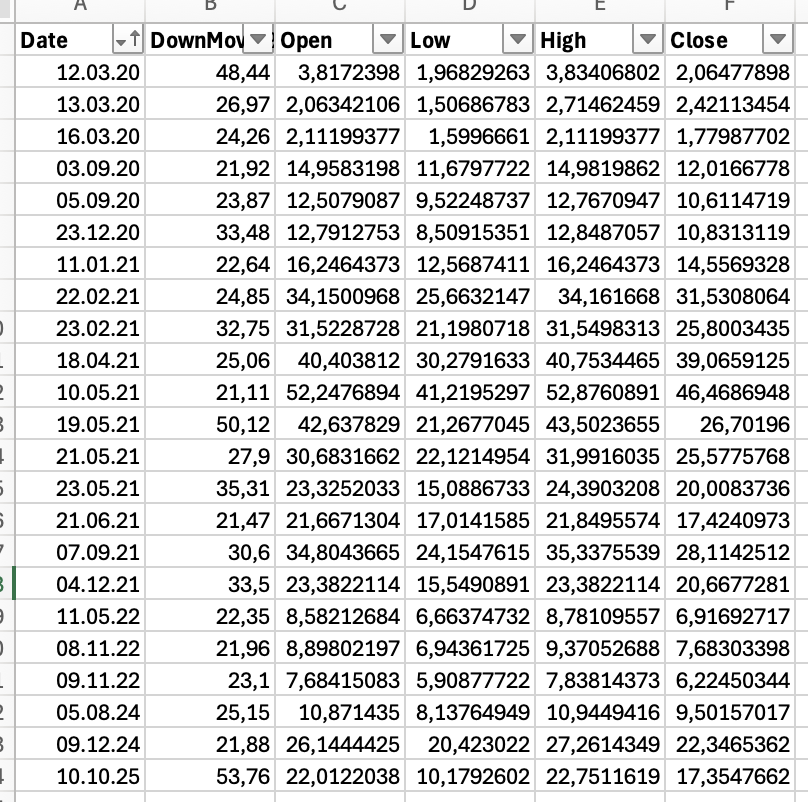

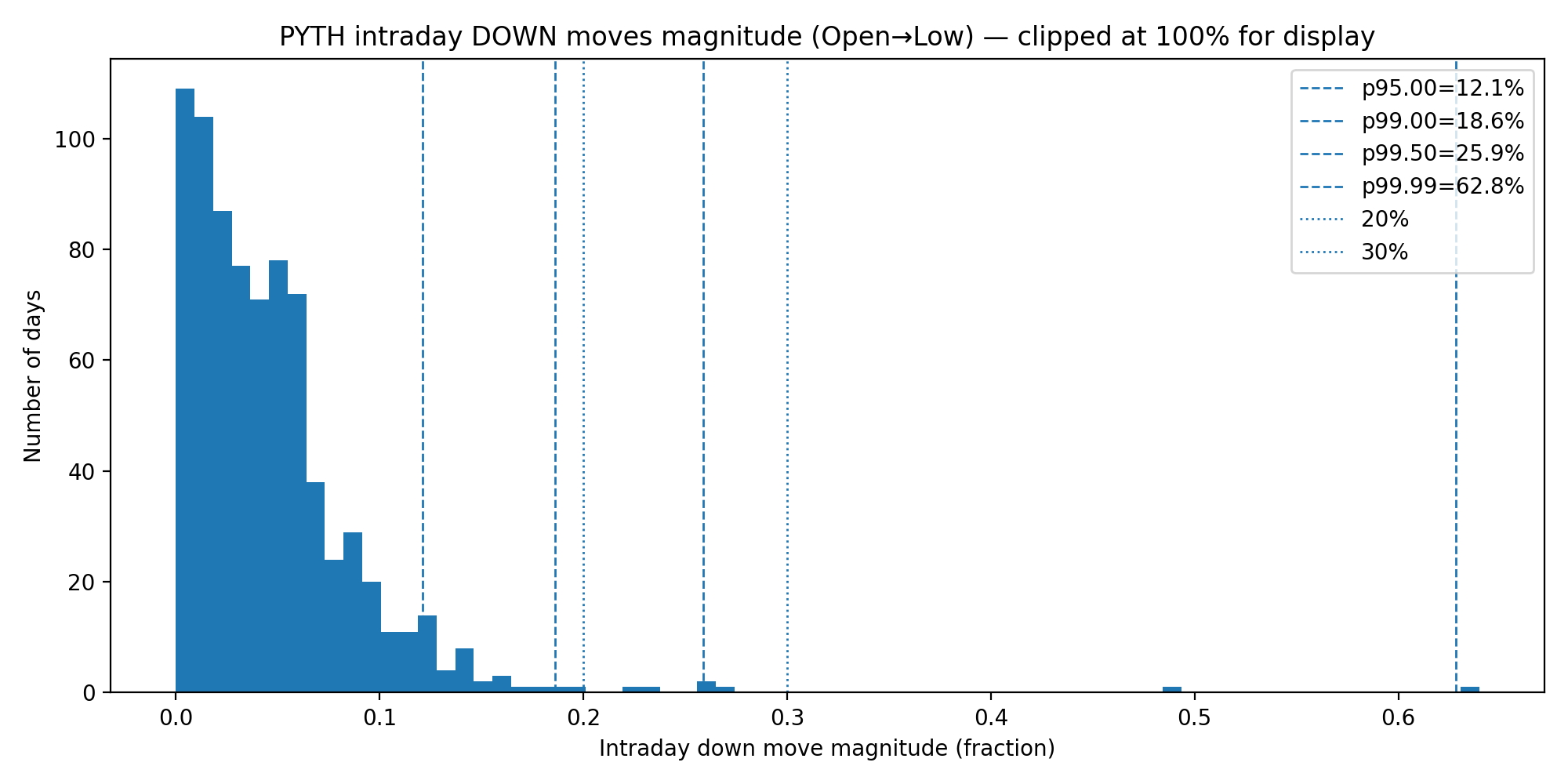

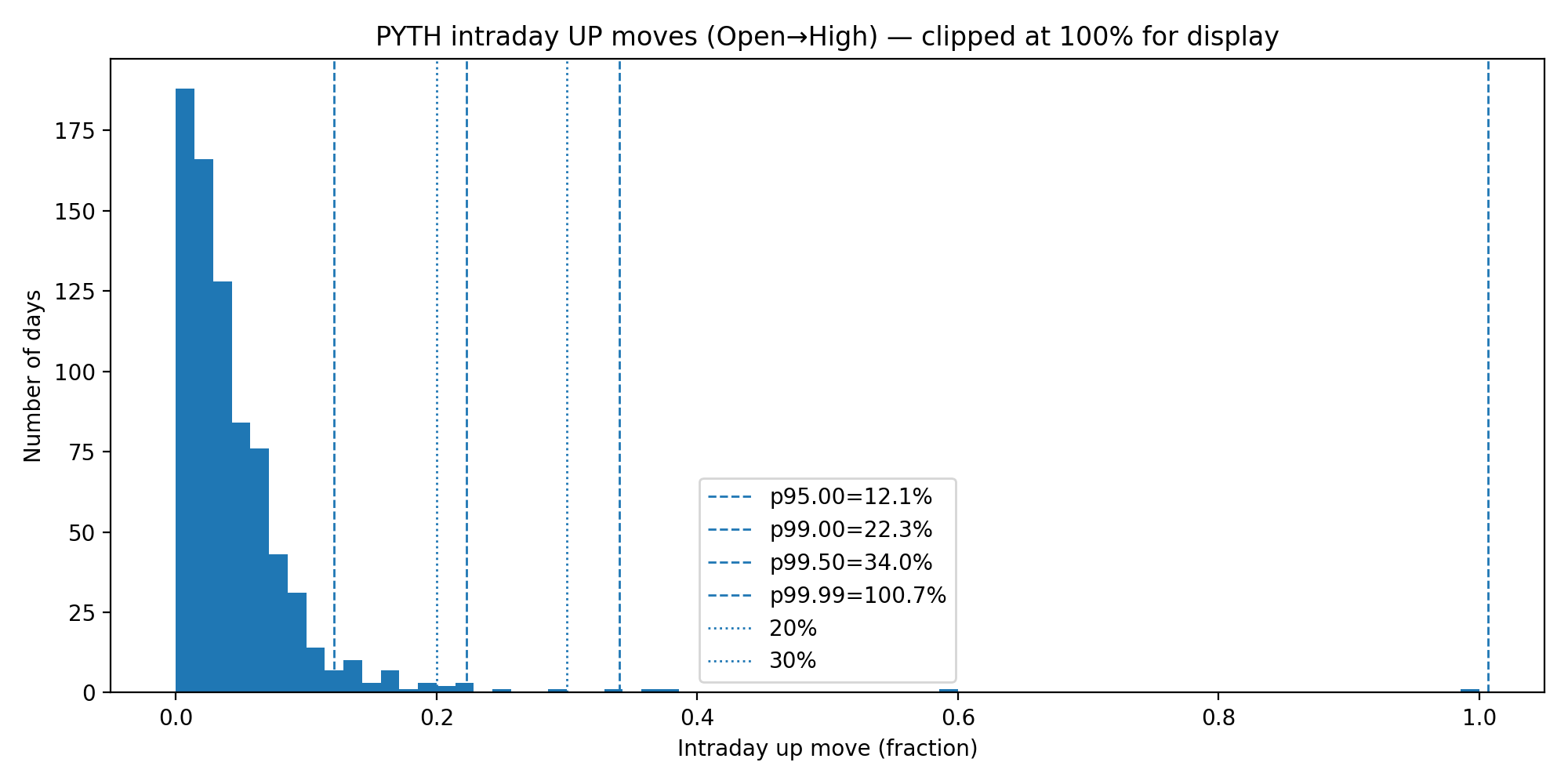

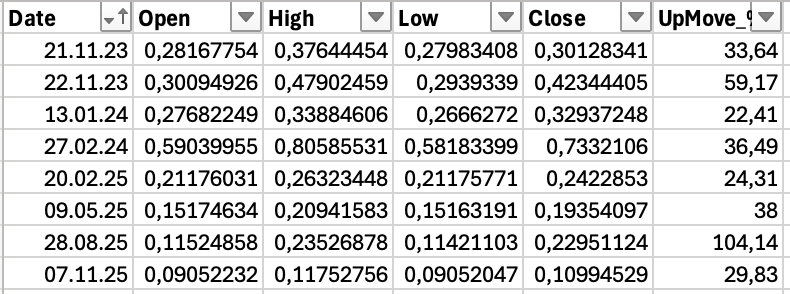

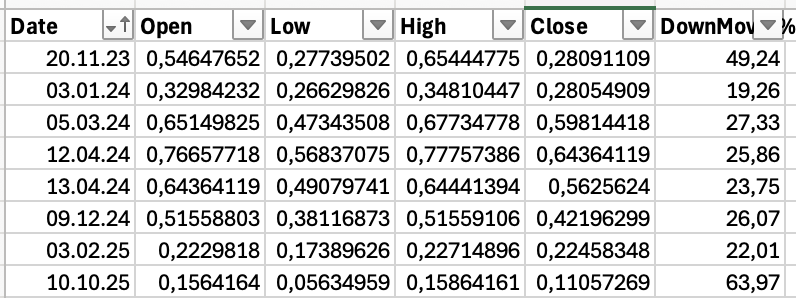

Below there is a detailed overview of all events > p99.00 for UP and DOWN moves.

Chainlink

Pyth

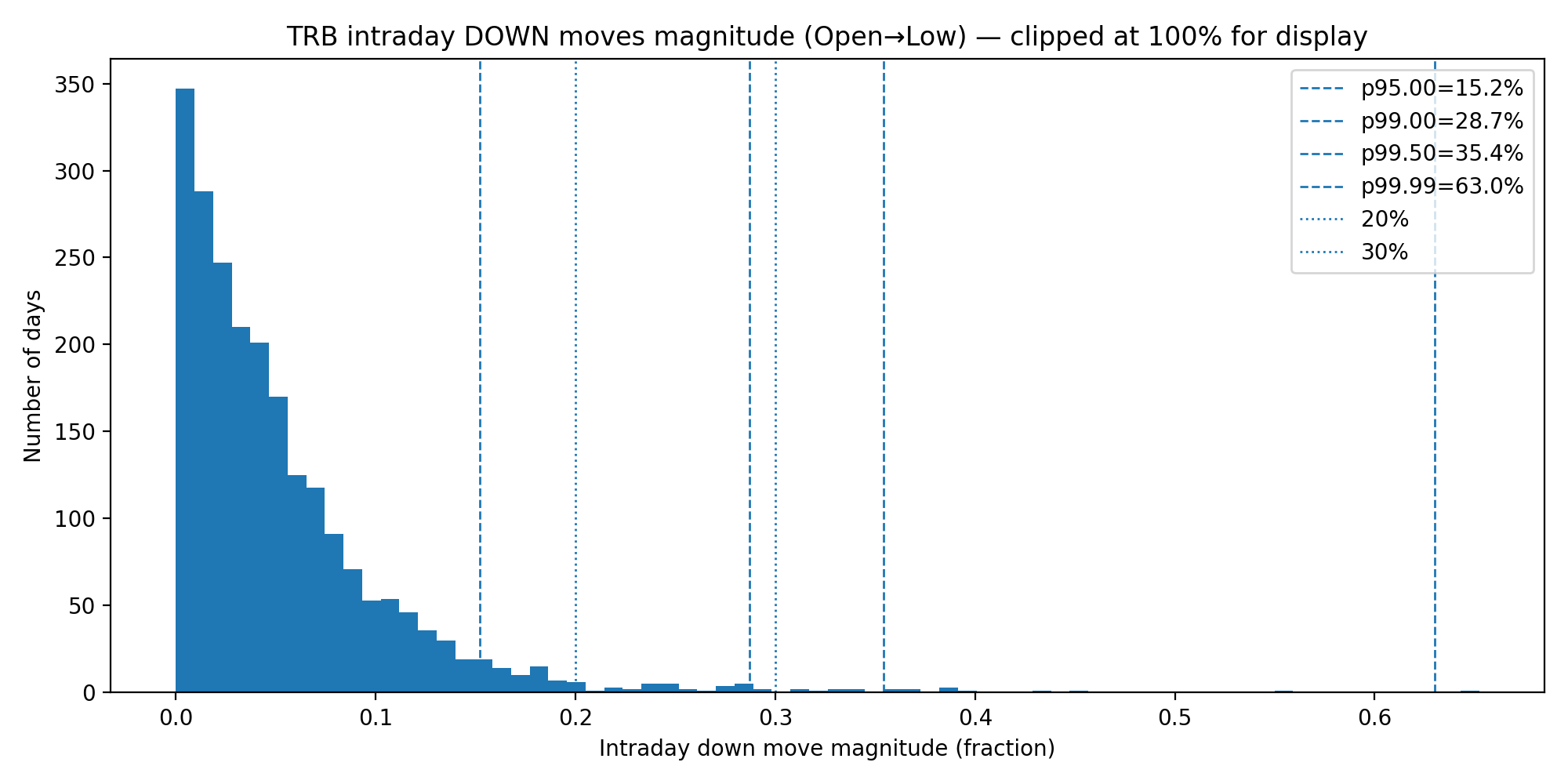

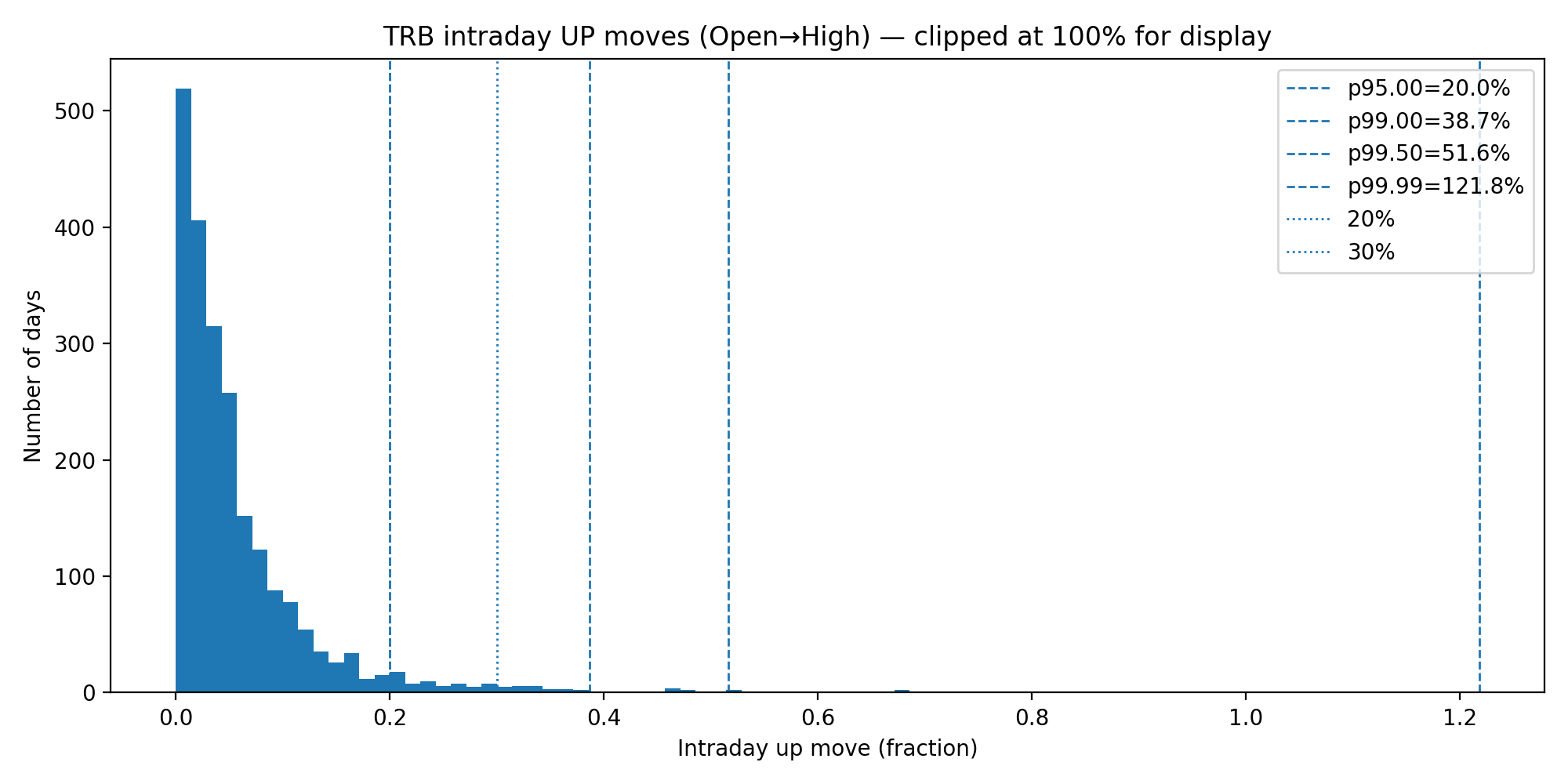

A key risk to Blocksize’s delta-neutral self-staking strategy, in particular to the hedging strategy, is extreme volatility. Extreme prices moves defined as >p99 (99th percentile or 1% tail event for either moves UP or moves DOWN) can either risk to liquidate short positions, if the move up is correlated and happens so quickly that no additional margin due to rebalancing can be provided, or force exchanges to close profitable short positions to ensure solvency of the exchange (Auto Deleveraging, also see Auto-Deleveraging Risk ). As per the data set above, on average for the selected assets, statistically a move UP and a move DOWN can be expected every 97 - 100 days; in other words, the strategy will experience 3 major UP moves AND 3 major DOWN moves per year. Looking at the data sample it can be stated that with higher market caps, institutional adoption and deeper liquidity, volatility will reduce making such moves UP or DOWN less aggressive.

Short Squeeze Circuit Breaker

A good protection for Short Squeezes leading to liquidation of Perp position is a safety program which will e.g. close short position if prices rise by 10% within a set short timeframe (e.g. Trigger price for SOL 150). The SPOT is than naked Long. However, if the price falls back to Trigger price of 150, the Hedge will be reopened again at exactly the exit price. If the price does not drop back to Trigger price, the Hedge will be reopened at a higher SOL price, realizing a gain in NAV.

Liquid Staking Tokens

Blocksize’s delta-neutral self-staking strategy utilizes Solana Liquid Staking Tokens (“LSTs”) such as bSOL and vSOL as a core building block to optimize capital efficiency, liquidity management, and validator economics. In addition, Blocksize may employ controlled looping strategies using LST/SOL pairs on protocols such as Kamino in order to increase effective staking exposure and align delegations toward Blocksize-operated Solana validators.

Blocksize deposits 100 SOL into LST (e.g. bSOL) and uses leverage of 7x via looping LST / SOL

Blocksize now has an exposure of 700 SOL in the LST pool

Blocksize directs SOL in LST pool to own validator now earning rewards and commissions for 700 SOL instead of 100 SOL

LST pool 1:1 matches delegations directed to Blocksize and delegates an additional 700 SOL to Blocksize’s validator

Blocksize’s validator now earns rewards and commissions for 1.400 SOL instead of 100 SOL.

While this structure materially enhances yield generation, it introduces a distinct set of risks that must be carefully understood and actively managed.

Liquid Staking Token (LST) Risks

Liquid Staking Tokens represent a claim on staked SOL plus accrued staking rewards, net of protocol fees and potential slashing. Although LSTs are designed to track the underlying value of SOL closely, they are not risk-free and may temporarily or structurally diverge from SOL.

The primary risks associated with LSTs include smart contract risk, validator performance risk, and redemption risk. LST protocols rely on smart contracts to manage minting, burning, delegation, and reward accounting. Any bug, exploit, or governance failure could impair the LST’s functionality or redemption mechanics. In addition, staking rewards and redemption value are dependent on validator uptime and correct behavior; extended downtime or slashing events may reduce the effective value of the LST.

Blocksize partners in particular with the team of The Vault (vSOL) and SolBlaze (bSOL) and joined their set of preferred validators. Both LSTs fulfill the above criteria, never experienced a compromise of their infrastructure or de-pegging event.

Risk Mitigation

Blocksize mitigates these risks by exclusively using established LST protocols with long operational track records, audited smart contracts, and high TVL. Furthermore, Blocksize operates its own Solana validator and actively directs delegations toward infrastructure under its direct operational control, reducing third-party validator dependency.

LST De-Peg and Secondary Market Discount Risk

LSTs may trade at a discount (or premium) to their on-chain redemption value on secondary markets such as decentralized exchanges. During periods of market stress, liquidity constraints, or forced deleveraging, these discounts can widen significantly.

Importantly, Blocksize distinguishes between market price risk and redemption value risk. While secondary market prices may temporarily deviate, the protocol-level redemption rate remains anchored to the underlying SOL plus accrued rewards. As long as redemption mechanisms function normally, sustained deep discounts do not necessarily translate into realized losses.

Blocksize in particular uses Kamino for looping since Kamino does not rely on Oracle prices from AMMs or DEXes, but uses the redemption rate of each pool by monitoring the circulating supply of the respective LST and the SOL in the respective LST Token contract.

Risk Mitigation

Blocksize mitigates de-peg risk by maintaining the operational ability to unwind positions via protocol redemption rather than relying solely on secondary market liquidity. That mean if the secondary market price of LST deviates for a longer period from the actual redemption rate, Blocksize can pay back the debt in SOL, receive the LST which then can be redeemed against SOL based on the Redemption rate, rather than closing the position based on market rates.

Blocksize actively monitors the health of each looped position and has automated mechanisms in place to unwind a lopped LST / SOL position immediately if a de-peg of the redemption rate occurs.

Interest Rate and Utilization Risk

Borrowing SOL on lending protocols exposes the strategy to variable interest rates that may spike during periods of high demand or market volatility. Elevated borrow rates can temporarily compress net yields or, in extreme cases, turn leverage uneconomic.

Risk Mitigation

Blocksize continuously monitors borrow utilization and net APY of looped positions. If interest rates become persistently unfavorable, leverage is reduced or positions are partially unwound or rebalanced to restore positive expected returns.

Slashing Risk

Risk Overview

Blocksize currently supports the following networks in which slashing resulting in a loss of Blocksize’s delta-neutral self-staking solution may occur:

Protocol | Slashing |

|---|---|

Solana | No Slashing |

Polygon | No Slashing |

Chainlink | 700 Link |

Pyth | max. 5% of staked Pyth |

Tellor | max. 100% of Reporters balance |

Chainlink Oracle:

Blocksize is one of 31 Node Operators securing the ETH / USD price feed on Ethereum in the Chainlink Network. When a valid alert is raised and a slashing condition is met (e.g. downtime, price accuracy, manipulation), Blocksize could see a portion of its staked LINK slashed as a penalty for failing to meet performance requirements. The Slashing penalty is 700 LINK for each event if a valid alerting condition is met.

Up to date no slashing event ever occurred since the introduction of Chainlink Staking. In addition, Blocksize has never experienced any downtime or pricing inaccuracy, which could have let to a slashing event since joining Chainlink in 2020.

Tellor Oracle:

Blocksize currently supports the ETH / USD price feed on Tellor Oracle. If questionable data is identified or a reporter is suspected of acting maliciously, any participant holding TRB on the network can initiate a dispute. There are three dispute categories: warning, minor, and major. This gives some flexibility to the ways dispute governance can be used to ensure smooth operation of the oracle.

Warning: The dispute fee / slashing amount is set at 1% of the reporter's bonded tokens. This is similar to the penalty for simple inactivity as a validator. The reporter will be jailed, but they may call `unjail` immediately to start reporting again with slightly reduced power while the dispute is settled.

Minor: The dispute fee / slashing amount is set a 5% of the reporter's bonded tokens. The reporter is jailed for 10 minutes.

Major: The dispute fee / slashing amount is set equal to the amount bonded by the reporter. The reporter will be jailed forever unless the vote result is

against.

No slashing event has been reported in the history of Tellor. In addition, Blocksize has never experienced any downtime or pricing inaccuracy, which could have let to a slashing event since joining Tellor in 2024.

Pyth Oracle:

Pyth's Oracle Integrity Staking (OIS) uses slashing as a penalty to enforce accurate price data from publishers. It reduces staked PYTH tokens (from both publishers' self-stake and delegated stakes in their pools) when verified data inaccuracies occur. The goal is to hold publishers accountable for faulty feeds that could harm DeFi protocols (e.g., causing preventable liquidations).

Key rules from the Pyth slashing rulebook:

Triggers — Slashing only applies if:

The aggregated Pyth price (for one or more assets/crosses) deviates by ≥250 basis points (2.5%) from the most liquid market venues' prices.

The deviation lasts ≥60 seconds.

Confidence intervals are normal (no abnormal flags).

Market conditions are normal (not macro-driven volatility or external shocks)

Maximum slash: 5% (500 bps) of the total staked amount in the responsible pools

Pythian Council investigates (using evidence from affected protocols, on-chain data, etc.), decides the slash rate (within cap), executes it by reducing pool stakes (no forced unstaking), and reports publicly. Slashing is decided within the same or next 7-day epoch. No historical Pyth slashing events have been reported and Blocksize is ranked amongst the global best performing Publishers.

Risk Mitigation

Blocksize is the market leader in accurate and reliable on-chain market data and node infrastructure. We have deployed multiple methods to ensure availability, accuracy and compliance of our systems:

Advanced monitoring of all price feeds against benchmark prices.

Immediate reporting and alerting of deviations (price fluctuations, staleness, downtime, deviations, etc.) via Redphone and internal alert system.

24/7 availability of market data and node infrastructure team.

Bullet-proof documentation of price feed quality against benchmarks in case an alert for slashing is raised.

Also, for Tellor Blocksize’s total stake is split across multiple single reporters, which report prices asynchronously to contain potential slashing risk.

Sources:

Pyth Slashing Rule Book: https://docs.pyth.network/oracle-integrity-staking/slashing-rulebook

Tellor Slashing: https://tellor.io/docs/

Chainlink Slashing: https://blog.chain.link/chainlink-staking-v0-2-overview/#staked_link_slashing_for_node_operator_stakers

Margin Risk

A key element of Blocksize’s delta-neutral self-staking strategy is hedging staked assets with perpetual future short positions. For opening and maintaining such positions, a maintenance margin needs to be provided on the exchange. During rapid price moves UP (see also Portfolio Allocation ) short positions will lose value and the account’s equity will be reduced. If the account’s equity < required maintenance margin, short positions will be liquidated leading to a naked longs position and directional exposure of the strategy.

Analyzing volatility of selected assets (see Portfolio Allocation) major UP moves (>p99) tend to occur in isolation for the respective asset and not as a correlated market wide event.

Risk Mitigation No. 1

For efficient margin management and capital efficiency, cross-margin across all major assets is being used for maintaining short positions. In addition, assets with lower market cap and less liquidity, which move UP more aggressive in a >p99 tail event, represent a smaller position in the portfolio.

Cross-margin reduces liquidation probability under idiosyncratic moves; however, cross-margin can also propagate stress across positions under correlated shocks. Therefore, leverage and margin ratio caps are enforced at the account level. Under observed historical distributions, current margin targets provide a buffer that is designed to withstand typical idiosyncratic tail moves (≥p99) without forced liquidation, subject to execution, liquidity and venue risk.

Risk Mitigation No. 2

Blocksize will keep the Cross Margin Ratio (Maintenance Margin / Account Equity) in the range of 20% - 25% and Cross Account Leverage capped at 3.5x. Automated Rebalancing and Alerting will occur if Cross Margin Ratio leaves the defined threshold.

Stress-testing the hedging strategy, the defined margin and equity requirements will secure the hedge against idiosyncratic pumps for each asset with >p99 (even without providing further margin through automated rebalancing). In addition the hedge is robust against a correlated move UP of ALL ASSETS in parallel within such a short timeframe that no additional margin can be provided of over 20%. No such event occurred in the observed sample for the assets analyzed. This indicates the event is rare in this dataset, but does not imply it cannot occur.

Risk Mitigation No. 3

In the unlikely event of a correlated move UP of all selected assets, an automated Circuit breaker will be activated, closing all short positions when the cross margin ratio > 80%. If the price then will decline back to the exit price / circuit breaker price, the short position will be reopened again. If prices remain above the circuit breaker level, the hedge will be re-established at the prevailing price with updated margin.

Liquidity Risk & Unlocking Periods

A key component in Blocksize’s delta-neutral self-staking strategy is staking (including oracle staking and validator staking). Staking improves expected returns but introduces liquidity constraints: Staked tokens cannot always be withdrawn or converted back to liquid collateral immediately. Many staking systems require an unbonding / unlock period during which the assets are illiquid and may also stop earning rewards or become subject to protocol rules (e.g., withdrawal queues, rate limits, or delayed settlement).

This creates a liquidity mismatch: the hedge (perpetual futures) is mark-to-market in real time, while parts of the underlying collateral (staked assets) may be locked for days to weeks. In stress scenarios, the strategy may need liquidity quickly to add margin and rebalance hedges, but the assets may not be instantly available.

During rapid market moves, short hedges can require additional margin. If liquidity is needed faster than staked assets can be unlocked, the strategy may face forced hedge reductions or liquidation risk, resulting in temporary directional exposure.

Asset | Activation period | Deactivation period | Reward payout frequency |

|---|---|---|---|

bSOL | none | none | 1 epoch (ca. 2 days) |

vSOL | none | none | 1 epoch (ca. 2 days) |

SOL | max. 1 epoch (ca. 2 days) | max. 1 epoch (ca. 2 days) | 1 epoch (ca. 2 days) |

Pyth | max. 1 epoch (7 days, every Thursday) | max. 1 epoch (7 days, every Thursday) | max. 1 epoch (7 days, every Thursday) |

TRB | none | 7 days | Instant (every successful report) |

POL | none | 4 days | Daily |

LINK | none | 28 days | 90 days cliff (one-off), thereafter daily |

Hyperliquid | none | none | Fund rate paid hourly |

Risk Mitigation

Blocksize separates assets into liquidity classes with predefined targets:

Tier 1 (Instant liquidity): stablecoins / cash equivalents held off-chain or in highly liquid venues, reserved for margin and operations (excluding margin already on exchanges).

Tier 2 (Near liquidity): liquid staking tokens (LSTs) and high-liquidity spot assets that can be sold quickly with acceptable slippage.

Tier 3 (Illiquid / locked): staked positions subject to unbonding.

In addition, Blocksize will always keep sufficient margin on Exchange for maintaining Short positions (see Margin Risk ) and diversfy Tier 1 Liquidity across multiple chains and sources to avoid congestion of networks for deposits on Exchanges for additional margin. When Tier Liquidity is held in Cash, such exchanges will be used where instant payments are enabled.

Liquidity Class | Target (of NAV) | Strategy Threshold (of NAV) |

|---|---|---|

Tier 1 (Instant liquidity) | 2% - 5% | min. 2% |

Tier 2 (Near liquidity) | 20% - 30% | min. 20% |

Tier 3 (Illiquid / locked) | 70% - 80% | max. 75% |

Auto-Deleveraging Risk

ADL (Auto-Deleveraging) is a last-resort solvency mechanism of Exchanges that forcibly closes profitable positions to offset bankrupt ones when liquidations and the Exchange can't cover deficits. Overall, it protects the Exchange but can "punish" winners during cascades, closing profitable positions and leaving traders with opportunity costs or “naked” Long-Positions.

Auto-deleveraging strictly ensures that the platform stays solvent. If a user's account value or isolated position value becomes negative, the users on the opposite side of the position are ranked by unrealized pnl and leverage used. Backstop liquidated positions have no special treatment in the ADL queue logic. The specific sorting index to determine the affected users in profit is (mark_price / entry_price) * (notional_position / account_value). Those traders' positions are closed at the previous mark price against the now underwater user, ensuring that the platform has no bad debt. (Source: https://hyperliquid.gitbook.io/hyperliquid-docs/trading/auto-deleveraging )

Auto-deleveraging is an important final safeguard on the solvency of the platform. There is a strict invariant that under all operations, a user who has no open positions will not socialize any losses of the platform. (Source: https://hyperliquid.gitbook.io/hyperliquid-docs/trading/auto-deleveraging )

Auto-deleveraging strictly ensures that the platform stays solvent. If a user’s account value (cross) or isolated position value becomes negative, users on the opposite side are ranked by unrealized PnL and leverage used. Backstop liquidated positions have no special treatment in the ADL queue logic. Hyperliquid publishes the sorting index used to determine which profitable accounts are deleveraged first:

SortingIndex = (mark_price / entry_price) * (notional_position / account_value)

For a short position this translates into the following actionable variables Blocksize can actively manage to reduce ADL risk:

Profitability / “distance in-the-money” of the hedge: the deeper in-the-money a short hedge becomes during a crash, the more likely it can be ranked for ADL (venue-specific).

Effective leverage: the higher cross-account leverage (notional_position / account_value), the higher the ADL selection pressure.

Risk Mitigation No. 1

As a hedge becomes deep in-the-money, Blocksize performs threshold-triggered “profit reset” rebalancing: a fraction of the short is closed and re-opened near the current mark to reduce the ranking pressure associated with highly profitable, aged hedges. This will reduce the Entry price. A rebalance is triggered if the positive PnL of a position expressed as ROE of margin exceeds 100%:

PnL (USD) > Margin (USD) → Rebalance

Execution policy: Upon trigger, Blocksize resets 25% of the hedge notional for the affected asset. To reduce execution costs, profit resets are capped at one reset per 24 hours per asset (cooldown).

Risk Mitigation No. 2

Blocksize limits cross-account leverage to max 3.5x and targets a Cross Margin Ratio (Maintenance Margin / Account Equity) of 20%–25% (see: Margin Risk). These measures reduce the probability of being highly ranked during ADL events.

In addition, Blocksize monitors crowding and stress indicators (where observable), including significant increases in Open Interest (OI), funding regime shifts, and leverage concentration. If these indicators signal rising systemic stress, Blocksize will proactively reduce venue concentration (shift hedge notional to secondary venues), and/or increase account equity buffers on venues to reduce SortingIndex pressure. (Source: https://hyperdash.com/?chart1=SOL ).

Risk Mitigation No. 3

Blocksize splits short hedges across multiple venues to avoid concentrated ADL risk on any single venue. All risk measures defined in Margin Risk (leverage caps, margin ratio targets, automated rebalancing and alerting) are applied consistently across venues.

Hedge continuity policy: at least 30% of aggregate hedge notional is maintained on a secondary venue (or alternative hedge instrument) under normal operations. The objective is to preserve partial hedge continuity even if the primary venue is impaired by ADL, outages, or other stress conditions.

Risk Mitigation No. 4

Some hedging venues have different default-management and loss-allocation designs, which can materially affect the likelihood and impact of forced hedge reductions during systemic crashes. While many crypto derivatives venues include auto-deleveraging or deleveraging mechanisms as a last-resort solvency tool, the trigger conditions and loss waterfalls differ by venue (e.g., use of insurance funds, backstop liquidity pools, and protocol-level deleveraging rules).

Blocksize therefore diversifies hedge execution across multiple venues and prioritizes (i) venues with transparent and well-capitalized risk waterfalls and (ii) venue designs that reduce single-point “hedge discontinuity” risk, subject to funding-rate economics and venue counterparty risk. Importantly, no venue can guarantee the complete absence of forced deleveraging in extreme conditions; the objective is to reduce both the probability and the portfolio impact via diversification and hedge continuity across independent venues.

Where feasible, Blocksize may also use CCP-cleared derivatives for hedging, which rely on a clearinghouse “default waterfall” (margin, guaranty fund, CCP resources, etc.) rather than exchange-level ADL ranking of profitable accounts.

During the October 10th 2025 crash, BitMEX and Lighter or the decentralized platforms dYdX and GMX did not experience any ADL events.

During extreme events of systematic failure, ADL cannot be fully eliminated on all Exchanges; the objective is to reduce its probability and, more importantly, reduce its impact by maintaining hedge continuity across venues and preserving sufficient liquidity buffers for rapid re-hedging. As additional safely measure, Blocksize will implement a circuit breaker to mitigate systematic stress to the strategy.

Funding Rate Risk

A key yield driver of Blocksize’s delta-neutral self-staking strategy is the funding (and basis spread) earned from short perpetual futures positions used to hedge spot/staked exposure. Funding payments are variable and market-driven. Funding rates can turn negative and remain negative for extended periods, in particular during risk-off regimes or when short positioning becomes crowded. Negative funding directly reduces strategy yield and, in adverse scenarios, can temporarily make the hedge leg a cost rather than a source of return.

In a simplified form, gross strategy yield for a hedged asset can be expressed as:

Gross APY ≈ Self-staking APY + Funding Rate (annualized).

Accordingly, when funding turns negative, the strategy may experience yield compression or, in extreme cases, negative carry on the hedge leg.

Funding may turn negative due to:

Risk-off positioning: increased demand for downside exposure and hedging; perps trade below spot.

Crowded shorts / basis dislocation: structural hedging flows depress perp pricing and funding.

Stress regimes: volatility spikes can coincide with liquidity deterioration, increasing both funding volatility and execution costs.

Negative funding is most harmful when it is:

Persistent: not a short-term blip, but a multi-day or multi-week regime.

Concentrated: driven by a small number of large positions/assets.

Coupled with liquidity stress: making resizing or venue rotation expensive.

Negative funding impacts the strategy through:

Direct yield reduction: funding payments become a recurring cost.

APY volatility: strategy returns become more dependent on staking rewards alone.

Execution and liquidity effects: regimes that create negative funding can also increase slippage for hedge adjustments.

Our mid-term analysis of Funding Rates during the period from 26.08.2025 - 22.02.2026 provides the following results:

Token | Exchanges | OI-Weighted Ann % | Simple Avg Ann % |

|---|---|---|---|

LINK | 18 | +5.74% | +5.18% |

BTC | 20 | +4.43% | +5.04% |

ETH | 10 | +4.17% | +3.42% |

TRB | 8 | +3.81% | -5.35% |

AVAX | 18 | +2.10% | -0.40% |

BAND | 11 | +1.21% | -3.19% |

SOL | 18 | +0.52% | -0.11% |

POL | 18 | -0.28% | -3.82% |

DIA | 7 | -5.10% | +1.49% |

BABY | 13 | -9.11% | -10.34% |

PYTH | 17 | -10.18% | -5.54% |

ATOM | 17 | -11.09% | -14.43% |

FLR | 7 | -19.69% | +10.20% |

API3 | 10 | -65.43% | -33.76% |

RED | 1 | -67.43% | -27.18% |

In general the time period before 10.10.2025 can be described as “risk-on” environment while the time period after 10.10.2025 can be described as “risk-off” environment. This finding is underlined by the following findings when comparing the OI-weighted annualized Funding Rate % before and after 10.10.2025.

Token | Before 10 Oct | After 10 Oct | Delta |

|---|---|---|---|

RED | -94.35% | -22.22% | +72.13pp |

FLR | -28.74% | -12.22% | +16.52pp |

PYTH | -16.72% | -2.28% | +14.44pp |

BTC | +3.82% | +4.68% | +0.86pp |

ETH | +5.55% | +3.47% | -2.07pp |

TRB | +5.45% | +2.73% | -2.72pp |

LINK | +8.58% | +3.81% | -4.76pp |

SOL | +4.98% | -2.30% | -7.28pp |

POL | +5.23% | -4.17% | -9.40pp |

AVAX | +8.28% | -3.08% | -11.36pp |

DIA | +2.04% | -9.99% | -12.03pp |

BAND | +10.31% | -5.00% | -15.31pp |

ATOM | +1.76% | -15.41% | -17.17pp |

BABY | +4.36% | -19.11% | -23.47pp |

API3 | -40.97% | -83.29% | -42.32pp |

Most tokens saw a significant shift from positive to negative funding after 10 Oct — the market went from net long to net short sentiment

RED, FLR, PYTH are the exceptions — they improved (became less negative) after the split

BTC and ETH held relatively stable, staying positive in both periods

BABY, API3 saw the steepest deterioration, suggesting heavy short positioning after Oct 10

The "before" period is shorter (~45 days) vs "after" (~135 days)

In “risk-on” environments the strategy is expected to return higher yield than during “risk-off” environments.

Looking at long-term funding rates in different regimes the following results can be for the OI-weighted mean funding rate across different trading venues:

Token | Bull 1 (Jan20-Dec21) | Bear 1 (Jan22-Feb23) | Bull 2 (Mar23-Sep25) | Bear 2 (Oct25-now) | Avg Bull | Avg Bear | Spread |

|---|---|---|---|---|---|---|---|

BTC | +16.3% | +3.5% | +8.4% | +4.3% | +11.6% | +3.7% | +7.9pp |

ETH | +20.7% | -0.3% | +8.6% | +2.8% | +13.5% | +0.5% | +12.9pp |

SOL | +22.2% | -17.9% | +8.8% | -4.0% | +13.3% | -14.3% | +27.6pp |

AVAX | +23.9% | -4.6% | +8.4% | -3.4% | +13.5% | -4.3% | +17.8pp |

ATOM | +38.7% | -3.4% | +3.8% | -17.9% | +17.7% | -7.1% | +24.8pp |

POL | -- | -- | +6.0% | -3.7% | +6.0% | -3.7% | +9.7pp |

BABY | -- | -- | -9.0% | -14.7% | -9.0% | -14.7% | +5.6pp |

LINK | +34.7% | +5.5% | +11.0% | +3.1% | +20.6% | +4.9% | +15.7pp |

PYTH | -- | -- | +6.7% | -1.7% | +6.7% | -1.7% | +8.4pp |

TRB | +24.6% | -2.7% | -34.5% | +3.0% | -14.5% | -1.2% | -13.2pp |

BAND | +35.0% | -10.1% | +10.5% | -0.6% | +19.1% | -7.6% | +26.8pp |

DIA | -- | +6.7% | +5.2% | -0.7% | +5.2% | +4.6% | +0.6pp |

FLR | -- | -- | -14.1% | -19.8% | -14.1% | -19.8% | +5.6pp |

RED | -- | -- | -21.1% | -13.0% | -21.1% | -13.0% | -8.1pp |

API3 | -- | +1.4% | -6.2% | -44.4% | -6.2% | -11.7% | +5.5pp |

Risk Mitigation No. 1 — Funding regime monitoring and alerting

Blocksize maintains continuous monitoring of funding rates across assets and venues and applies threshold-based alerting. Monitoring includes:

current and rolling-average annualized funding rates,

funding sign flips (positive → negative),

persistence indicators (duration of negative streaks)

Risk Mitigation No. 2 — Position sizing linked to funding conditions

Position sizes are dynamically adjusted based on funding conditions. If funding becomes persistently unfavorable, Blocksize reduces exposure in the affected asset(s) and prioritizes allocations toward assets with (i) more resilient funding profiles and/or (ii) higher staking income components. This reduces portfolio sensitivity to prolonged negative funding regimes.

Risk Mitigation No. 3 — Venue diversification and hedge routing

Funding can be venue-specific. Blocksize therefore diversifies hedge execution across multiple venues and, where feasible, routes hedge notional to the venue offering superior funding economics subject to liquidity, counterparty limits, and operational constraints. This mitigates the risk that a single venue dislocation drives portfolio-wide funding underperformance.

Risk Mitigation No. 4 — Funding “kill-switch” and de-risk procedures

Blocksize defines escalation thresholds under which the strategy reduces risk when funding becomes structurally negative. Typical actions include:

reducing hedge notional in the affected asset(s) (within defined delta tolerance),

shifting exposure to higher-liquidity assets,

temporarily pausing incremental scaling into assets with persistently negative funding.

holdings stablecoins

Funding-rate risk is treated as a portfolio risk factor. Blocksize enforces concentration limits per asset and links allocation to liquidity and unwind capacity. This reduces the probability that a single funding regime shift dominates portfolio performance and improves the ability to resize positions during stressed conditions.

Counterparty Risk

A key operational dependency of Blocksize’s delta-neutral self-staking strategy is the use of third parties to custody collateral, execute hedges and perform staking / looping via Smart Contracts. Counterparty risk is the risk that one of these venues or protocols fails to perform as expected due to insolvency, operational outages, hacking, withdrawal restrictions, legal/regulatory actions, or extreme market conditions.

Counterparty risk cannot be eliminated; the objective is to reduce both its probability and impact through diversification, conservative exposure limits, operational controls, and pre-defined stress procedures. Blocksize will always prefer transparent, decentralized applications where governance, mechanisms and procedures are open source, verifiable in the source code and battle-tested in practice through a long and robust track-record complemented by regular 3rd Party Audits from reputable auditors.

Consistent with Blocksize’s risk posture, the strategy prioritizes systems with:

Long-standing track record

High TVL and deep liquidity

Long history of audits and fixes in the codebase

Active community and ongoing maintenance

Transparent, verifiable mechanisms

Clear regulatory status (where applicable)

This selection bias is a deliberate mitigation: it reduces both the probability of catastrophic protocol failure and the likelihood of severe impairment during market stress.

Risk Mitigation No. 1

Blocksize maintains an internal allowlist of approved exchanges, protocols and smart contracts. A venue or protocol is eligible only if it meets minimum standards across the following dimensions:

Track record and resilience

Demonstrated long-standing operating history through multiple volatility regimes, including prior market stress events.

Evidence of robust default management and incident handling (e.g., liquidations functioning as designed, orderly recovery from outages).

Economic security and scale (TVL / depth)

For on-chain protocols: sufficiently high and stable TVL and deep liquidity relative to expected position sizes, reducing the risk of destabilizing slippage and fragile liquidity.

For centralized venues: meaningful and verifiable liquidity and risk buffers (e.g., insurance fund design, liquidation engine maturity).

Security posture and audit history

Multiple, reputable third-party audits and a clear history of remediation and fixes in the codebase.

Preference for contracts with a long history of security review, bug bounties and responsible disclosure.

Clear upgrade and admin key controls (including timelocks, multi-sig governance, and transparent upgrade policies).

Active community and governance quality

Evidence of an active developer and user community, frequent peer review, and ongoing maintenance.

Transparent governance processes with clear accountability, change control, and public communication.

Transparency and verifiability

Preference for open-source, verifiable smart contracts and documented mechanisms (risk parameters, liquidation logic, oracle design, fee model).

Public reporting of incidents and post-mortems where applicable.

Clear regulatory status and operational compliance

For centralized venues and service providers: clear jurisdictional setup, compliance posture, and transparent legal terms.

Avoidance of venues with ambiguous legal status, unresolved enforcement actions, or persistent uncertainty around custody and client asset segregation.

Only venues/protocols that meet these standards are used in production. Exceptions require explicit risk approval and typically reduced exposure limits.

Risk Mitigation No. 2

Even high-quality counterparties can fail under stress. Blocksize therefore enforces strict concentration limits:

Maximum counterparty exposure per venue/protocol: capped at ≤ 25% of NAV),

Diversification across venues: hedges are split across multiple venues to reduce hedge discontinuity risk from a single venue (e.g., ADL, outage, withdrawal freeze). LST are allocated across multiple providers.

Position sizing linked to liquidity: expected unwind size must be supportable under conservative slippage assumptions, particularly for smaller market cap assets.

This ensures any single counterparty failure results in a manageable drawdown rather than an existential loss.

Risk Mitigation No. 3

Blocksize operates 24/7 monitoring of critical infrastructure as part of their Node Operations.

Centralized venues

Monitor: API reliability, withdrawal status, liquidation engine performance signals, major OI spikes, extreme funding shifts, venue announcements, and abnormal spreads.

Actions: reduce exposure, shift hedge notional to secondary venues, increase buffers, or proactively de-risk if indicators deteriorate.

On-chain protocols / Layer 1

Monitor: TVL trends, pool depth, depeg metrics (for LSTs), oracle integrity signals, governance proposals affecting risk parameters, contract upgrade events, and chain congestion. For Layer 1 monitor operational status and protocol metrics.

Transparency

Blocksize, as a true believer in decentralization and transparency, designs the underlying delta-neutral self-staking strategy so that sophisticated users and independent third parties can verify all relevant details: what assets back the strategy, where they are held, what risks are being taken, and whether the hedge and collateralization remain within defined limits.

Our transparency philosophy is informed by the best practices we see emerging in market-neutral dollar strategies: combining real-time visibility, independent attestations, and clear, auditable reporting—so trust is not “asked for,” but continuously earned.

What “transparency” means for Blocksize

Transparency is not a single dashboard metric. It is a set of concrete disclosures that allow stakeholders to assess solvency, custody safety, hedge integrity, and operational discipline.

Real-time visibility into reserves, liabilities, and risk metrics

Blocksize will provide a transparency view that allows stakeholders to understand, at minimum:

the strategy’s net asset value,

the composition of backing assets (spot/staked positions),

the derivative hedge notional and key risk limits (e.g., delta tolerance, leverage and margin ratios), and

summary exposures by venue (concentration and counterparty limits).

This approach follows the principle that users should be able to independently assess solvency and positioning through up-to-date, verifiable information.

Onchain transparency where feasible (verifiable addresses and flows)

Where assets are held onchain, Blocksize will publish relevant wallet addresses and enable users to verify balances and movements via public block explorers. This supports real-time auditability of custody and operational flows.

Custody attestations where addresses cannot be fully published

In institutional custody setups, assets may be held in structures where publishing a single onchain address is not always feasible (e.g., omnibus arrangements). In these cases, Blocksize will rely on periodic custodian attestations (at least monthly) to confirm the existence and value of backing assets held with custody partners—so transparency is maintained even when onchain address disclosure is constrained.

Exchange risk reduction through off-exchange custody and settlement controls (where applicable)

Where Blocksize requires interaction with centralized liquidity venues, Blocksize will prefer architectures that minimize “assets sitting on exchange” risk—e.g., custody and settlement workflows that keep beneficial ownership outside the exchange where possible and enable frequent settlement of derivatives PnL to reduce the impact of exchange failure between settlement cycles.

Verifiability of hedge positions (derivatives transparency)

Blocksize will disclose the principles and metrics that demonstrate hedge integrity (e.g., delta exposure limits, hedge notional vs spot/staked notional, margin health). Where feasible, Blocksize will also pursue mechanisms that allow third parties to validate the existence of hedge positions without compromising operational security—consistent with the industry direction of enabling independent verification of hedging derivatives positions.

Independent assurance: audits, attestations, and reporting cadence

To supplement onchain data and real-time views, Blocksize will publish periodic transparency materials that are designed for institutional review:

Reserve and process audits: routine independent reviews of reserve sufficiency and operational processes, with reports made available to stakeholders.

Custody attestations: periodic confirmations by custody partners regarding assets held, especially where address disclosure is limited.

Transparency reports: regular summaries of reserve composition, hedge posture, key risk metrics, and any deviations or incidents, including corrective actions taken.

Blocksize’s goal is to set a transparency standard that matches the expectations of institutional allocators: verifiable backing, clear custody controls, measurable hedge integrity, and continuous reporting. Transparency is treated as a core risk control—because in market-neutral strategies, confidence is earned through what can be independently verified, not what is promised.

Scalability of Strategy

Asset | Market Cap (in USD) | Staked Tokens in % of Market Cap | Volume 24h2 | TOP 1 Volume 24h SPOT (in USD) | Market share TOP 1 Exchange of Volume 24h SPOT in %2 | 2% / -2% Depth SPOT2 (in USD) | Volume 24h PERP2 (in USD) | Open Interest PERP2 (in USD) | Market share TOP 1 Exchange of Volume 24h PERP in %2 | Self-Staking APY | Comment |

|---|---|---|---|---|---|---|---|---|---|---|---|

SOL | 69.330.000.000 | 69,1% | 6.305.751.000 | 1.477.065.406 | 11,5% | 21.554.967,00 / 20.102.969,00 | 11.283.039.671 | 3.442.619.347 | 13,0% | 5,9% | |

LINK | 8.370.000.000 | 5,7% | 494.034.000 | 136.447.995 | 11,6% | 10.476.044,00 / 12.121.781,00 | 562.648.714 | 274.894.943 | 14,4% | 14,45% | Remaining allotment 62.951.00 LINK |

PYTH | 332.880.000 | 29,5% | 20.292.000 | 5.583.427 | 10,9% | 284.468,00 / 699.089,00 | 55.963.334 | 12.218.222 | 18,1% | 10% | |

TRB | 52.880.000 | 1,9% | 1.872.000 | 6.836.580 | 13,9% | 259.980,00 / 316.954 | 35.044.564 | 16.247.400 | 14,3% | 80% | |

POL | 1.290.000.000 | 34,6% | 77.537.000 | 16.607.739 | 9,5% | 1.103.239,00 / 1.184.329 | 80.651.834 | 40.832.909 | 11,5% | 3,3% | |

API3 | 35.120.000 | 0,5% | 14.466.000 | 1.602.986 | 6,6% | 189.235,00 / 252.688,00 | 16.605.067 | 7.337.510 | 18,4% | 60,5% | Remaining allotment 6.500.000 API3 |

BAND | 49.300.000 | 53,0% | 5.104.000 | 1.543.966 | 10,7% | 381.090,00 / 380.215,00 | 5.999.554 | 2.800.914 | 12,2% | 16,7% | |

DIA | 30.860.000 | 3,6% | 2.483.000 | 1.881.358 | 39,0% | 202.752,00 / 98.629,00 | 8.304.413 | 1.875.950 | 69,2% | 30% | |

RED | 72.280.000 | n/a | 5.000.000 | 2.893.157 | 20,1% | 203.744,00 / 325.743,00 | 10.247.218 | 5.713.891 | 21,5% | 4,0% | |

BABY | 49.500.000 | 19,8% | 8.200.000 | 3.433.497 | 16,0% | 481.203,00 / 1.167.003,00 | 9.857.560 | 2.626.831 | 53,6% | 13,4% | |

ATOM | 1.100.000.000 | 60,5% | 54.240.000 | 11.230.673 | 6,7% | 657.213,00 / 775.021,00 | 60.461.628 | 65.764.847 | 13,1% | 18,7% | |

AVAX | 5.030.000.000 | 46,2% | 335.020.000 | 88.273.956 | 9,3% | 3.574.244,00 / 4.197.229,00 | 484.507.428 | 192.333.916 | 14,1% | 5,5% | |

ETH | 348.980.000.000 | 30,2% | 31.260.000.000 | 4.966.022.920 | 5,0% | 42.984.396,00 / 45.700.949,00 | 50.946.156.995 | 16.632.029.180 | 11,3% | 2,4% | |

FLR | 855.780.000 | n/a | 6.350.000 | 3.286.198 | 15,7% | 632.204,00 / 686.695,00 | 7.924.036 | 1.300.009 | 66,8% | 60% |

Notes:

Table as of 26th January 2026

Volume and market depth has been calculated based on Binance, Bybit, OKX, Hyperliquid and Coinbase and the tokens USDC, USDT and USD pair for the 5 Exchanges with highest Volume / market depth.

Sources: Coinmarketcap.com, stakingrewards.com

Statistical Model for different TVL scenarios

Model parameter:

Max. exposure of Total Open Interest for each asset: 25%

Market depth +2% / -2% and 24h trading volume must allow a complete opening / closure of each position within a period of 30 days without market impact > 1% slippage

No position can exceed 25% of overall portfolio allocation

Cross account leverage for Perpetual Future Margin is max. 5x. Margin position is part of the overall portfolio.

Weekly compounding of rewards.

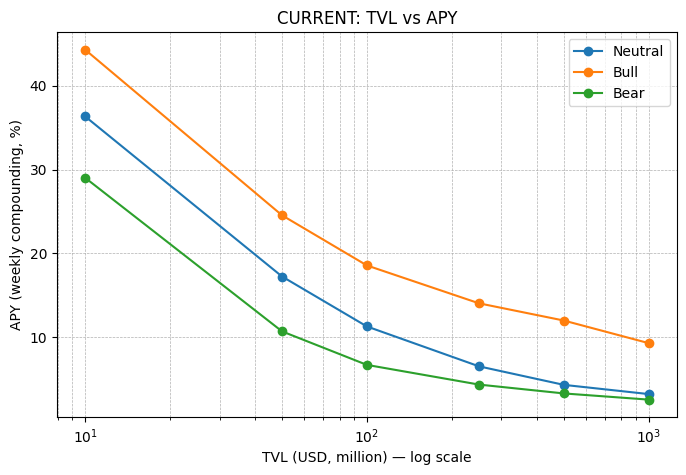

In the following analysis the above model parameters are static whereas the Funding rate is variable across different market regimes. We have modeled the portfolio allocation and corresponding APY for the TVL Levels 10m USD, 50m USD, 100m USD, 250m USD, 500m USD, 1bn USD

Neutral Funding rate regime with Funding Rates being neutral = 0% p.a or if both bull and bear are negative the mean between them

OI-weighted mean Funding Rate of Bull-market regimes during the period 01 2020 - 02 / 2026

OI-weighted mean Funding Rate of Bear-market regimes during the period 01 2020 - 02 / 2026

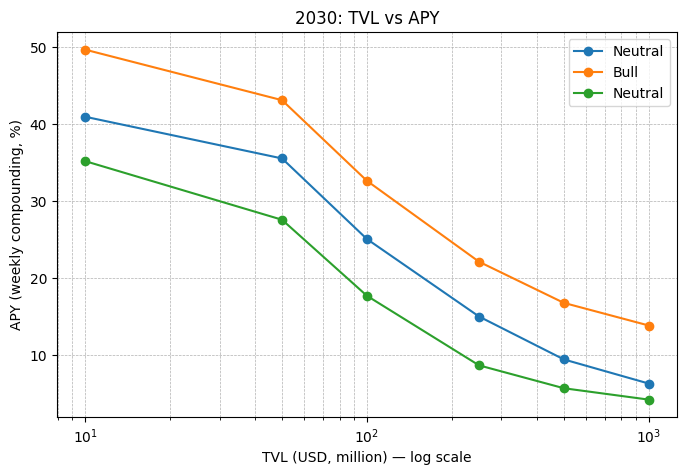

Affects to further take into account with increasing maturity of the market:

We expect the Oracle market to grow with > 40% CAGR significantly supporting the scalability of the strategy in the next 5 years

Chainlink eventually will roll-out Staking across all price feeds allowing for more capital allocations by Node Operators

Market depth and OI will significantly increase

Volatility of assets will reduce

Volatility in funding rates will reduce

If modeled with a 40% CAGR of static model parameters the strategy outputs will changes as follows (ceteris paribus):

Funding rate analysis

Token | Bull 1 (Jan20-Dec21) | Bear 1 (Jan22-Feb23) | Bull 2 (Mar23-Sep25) | Bear 2 (Oct25-now) | Avg Bull | Avg Bear | Spread |

|---|---|---|---|---|---|---|---|

BTC | +16.3% | +3.5% | +8.4% | +4.3% | +11.6% | +3.7% | +7.9pp |

ETH | +20.7% | -0.3% | +8.6% | +2.8% | +13.5% | +0.5% | +12.9pp |

SOL | +22.2% | -17.9% | +8.8% | -4.0% | +13.3% | -14.3% | +27.6pp |

AVAX | +23.9% | -4.6% | +8.4% | -3.4% | +13.5% | -4.3% | +17.8pp |

ATOM | +38.7% | -3.4% | +3.8% | -17.9% | +17.7% | -7.1% | +24.8pp |

POL | -- | -- | +6.0% | -3.7% | +6.0% | -3.7% | +9.7pp |

BABY | -- | -- | -9.0% | -14.7% | -9.0% | -14.7% | +5.6pp |

LINK | +34.7% | +5.5% | +11.0% | +3.1% | +20.6% | +4.9% | +15.7pp |

PYTH | -- | -- | +6.7% | -1.7% | +6.7% | -1.7% | +8.4pp |

TRB | +24.6% | -2.7% | -34.5% | +3.0% | -14.5% | -1.2% | -13.2pp |

BAND | +35.0% | -10.1% | +10.5% | -0.6% | +19.1% | -7.6% | +26.8pp |

DIA | -- | +6.7% | +5.2% | -0.7% | +5.2% | +4.6% | +0.6pp |

FLR | -- | -- | -14.1% | -19.8% | -14.1% | -19.8% | +5.6pp |

RED | -- | -- | -21.1% | -13.0% | -21.1% | -13.0% | -8.1pp |

API3 | -- | +1.4% | -6.2% | -44.4% | -6.2% | -11.7% | +5.5p |

Notes:

For the above scenario analysis only the SOL funding rates from Bull 2 (Mar23-Sep25) and Bear 2 (Oct25-now) have been included since they are considered representative given the increased maturity of this asset compared to the first bull / bear cycle

For TRB the market dynamics have changed. Hence for bull-market regime 6%, neutral 0% Funding rate and bear market -6% Funding rate will be assumed.

In case that both Avg. Bull and Avg. Bear Funding Rates are negative the model will assume the mean between both regimes as neutral funding rate regime. For all other token 0% Funding rate will be assume as neutral market regime.

Launching BlockUSD

Blocksize plans to make their delta-neutral staking-strategy available through their own DeFi native Token BlockUSD. Blocksize will leverage their existing relationships to Decentralized Applications to grow adoption in the DeFi Ecosystem, list BlockUSD on major AMMs and enable leveraged strategies / looping to amplify yield of BlockUSD.

Blocksize will charge a 2% Management Fee p.a. and a 20% Performance Fee. The strategy will allow for monthly redemption and reinvest staking rewards.

After the launch of BlockUSD, Blocksize will also offer BTC, ETH and SOL denominated strategies with BlockBTC, BlockETH and BlockSOL. This will allow investors to maintain a directional exposure in the asset, but benefit from Blocksize’s delta-neutral self-staking strategy, offering higher diversification and yield compared to native staking of such assets.